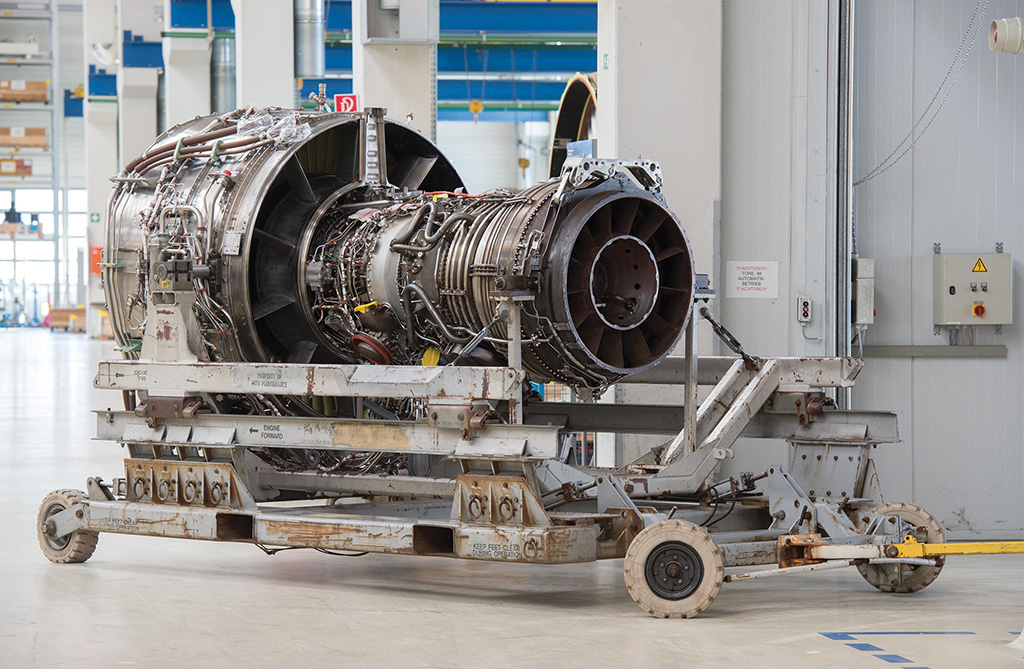

Airlines are still learning about the reliability of new-technology engines—and how many spares they need.

Spare engines provide both operational and financial flexibility for airlines. Their primary role is to keep aircraft flying when standard engines are undergoing overhaul or are out of service for other reasons. Accordingly, demand for spare engines rises during busy maintenance periods and falls when engine shop visits diminish—such as during the early part of the COVID-19 pandemic. Such crises also stretch airline balance sheets, prompting some operators to boost liquidity by selling sidelined assets such as aircraft and spare engines.

Given the brisk recovery of short- and medium-haul passenger markets through 2022, many airlines have had to adjust their spare-engine strategies to cope with resurgent maintenance demand.

“As we were able to reduce shop visits to generate cash savings during the crisis, the shop visit schedule is condensed within the next years for some engine types,” notes Michael Kaye, Lufthansa Group’s managing director of engine management.

Kaye also confirms that the German airline group is seeing demand for spare engines changing. “During the pandemic, fewer spare engines were needed due to reduced operational demands,” he continues. “Currently, Lufthansa Group airlines see an increase in demand on specific engine types.”

Tom Barrett, president and CEO of engine lessor Engine Lease Finance Corp. (ELFC), supports this view. “For some engine types we are heading back to equilibrium in the market supply,” he says. “As ever in a diverse industry, with different models and regional differences, there are variations of this equilibrium across the engine and regional sectors,” he says.

Obviously, each airline’s spare-engine requirement will differ according to the type and age of equipment it operates, and to the traffic profile of its particular market. In 2022, for example, a Chinese low-cost carrier (LCC) needed fewer spares than a European LCC of equivalent size.

Globally, however, Aviation Week data provides some insight into how spare-engine demand will wax and wane. For the CFM56, for example, Aviation Week’s 2023 Commercial Fleet & MRO Forecast predicts about 2,300 engine shop visits in 2023, rising to a peak of about 3,000 two years later. Visits for the competitor engine IAE V2500 also will peak in 2025, with almost 1,000 shop visits that year.

The most popular widebody engines in service in 2023 are expected to be General Electric’s CF6 and GE90, numbering 2,600 and 2,200, respectively. Aviation Week predicts about 500 CF6 shop visits in 2023, rising to a peak of 730 in 2025, while GE90 visits are forecast to reach a peak of roughly 500 in 2029 from over 400 in 2023.

In contrast, the new-generation narrowbody engines, the CFM Leap and Pratt & Whitney PW1000G, will have very few shop visits over the next few years given their youth. This makes spare-engine demand for such types harder to predict, hinging as it does on the unscheduled removals occurring due to early life issues of both types. Thus, airlines face a challenge in ascertaining how many spares they need—the spare-engine ratio—for a given number of in-service new-technology engines.

“For the newer technology that is still entering into service, the airlines and OEMs providing support to their programs have a much more difficult time estimating the correct ratios,” Barrett says. “However, in the long run, as the operating reliability builds, we would expect to see a return to ‘normal’ spares ratios, and as ever, these will be provided from a combination of OEM support, operating lessors and airlines’ own access to financing.”

Kaye says Lufthansa “is continuously improving its spare-engine ratio to ensure a stable operation.” He adds that since 2022, the group has centralized engine planning for all its airlines: Austrian Airlines, Brussels Airlines, Lufthansa, Swiss and the LCC Eurowings.

Engines As Assets

During the pandemic, as cash flows have been savaged by the collapse in passenger services, some airlines have leaned on their inventories of spare engines to boost liquidity via sale-and-leaseback (SLB) deals.

In November 2020, for example, SMBC Aero Engine Lease signed an SLB deal with Cebu Pacific covering eight CFM56-5B4 spare engines. Over the next year, it also conducted a CFM Leap SLB transaction with Indian carrier Vistara, while Vietnam-based LCC Bamboo Airways sold and leased back from ELFC its first CFM Leap spare engine.

The biggest transaction in this space, however, occurred in the summer of 2022, when Apollo Global Management invested $500 million into an affiliate of Air France-KLM dedicated to owning spare engines for the airline group’s maintenance arm, AFI KLM E&M.

The extent to which airlines cash in on their spare-engine inventories, and the balance they strike between owned and leased engines, depends on circumstance and strategy. In Air France’s case, it courted private equity investment to pay back state aid.

The Lufthansa Group also has received huge state loans during the pandemic, but Kaye says it still owns a majority of spare engines for its “baseline” demands, with additional needs evaluated on a case-by-case basis. “The owned engines provide a high degree of operational flexibility,” he observes.

In the past, full-service carriers such as Lufthansa have tended to own equipment such as aircraft, while LCCs have tended to lease them, notwithstanding some significant exceptions to that rough rule of thumb. However, Barrett says this distinction does not apply to spare engines any longer.

“While there would have been quite a difference in the past between legacies and LCCs, we are seeing the differences diminish,” he says. “Instead of the type of airline being important, I think it is down to the balance sheet and relative ease of access to capital that drives the decision to lease or own spare engines.”

Brazilian carrier Gol chose the ownership option last October, agreeing to an $80 million financing with Apollo’s aviation lending unit, Apollo PK AirFinance, for the airline to buy one new Leap 1B and eight new CFM56-7B engines.

Barrett also observes that opportunities to purchase spare engines from airlines during the pandemic have not been as numerous as ELFC had expected. “A little surprising to us, given the nature of the crisis, was that few airlines chose to use their owned engines to generate liquidity,” he says, adding: “In our opinion it suggests the issues faced were so great that rebuilding their balance sheets was secondary, at least initially.”

Supply Chain Impact

As airlines sought to rebuild passenger capacity through 2022, they faced supply chain pressures from two directions: the OEMs and the aftermarket. Delays to new aircraft deliveries meant that they had to operate older aircraft longer, which generated different spare-engine requirements than they had anticipated. At the same time, MRO capacity problems resulting from labor and material shortages led to longer turnaround times for work such as engine overhauls, which again boosted demand for spare engines.

“The technical fleet management of Lufthansa Group airlines is in continuously close contact with the OEMs and MROs to proactively manage shortages and reduce operational impacts to a minimum,” Kaye says. “Adjustments on spare-engine quantity and strategy are decided specifically per engine type.”

Barrett, meanwhile, confirms that supply problems have been good for business. “With the recovery coming at a much faster pace than was anticipated for many regions, and the supply chain issues for MROs and OEMs, we are seeing a good bounce-back in terms of demand,” he says.

Although operating leasing can help airlines negotiate a tight maintenance market for current-generation equipment, it is less useful to mitigate delivery delays of the newest engines—simply because there are far fewer of these available for lease. A lack of new-technology spare engines has hit operators in many parts of the world, notably in India, where carriers have even been forced to ground aircraft.

Commenting on the most recent results of IndiGo, India’s largest airline, CEO Pieter Elbers says: “One of the key aftereffects of the pandemic in the aviation industry are the supply chain disruptions in aircraft manufacturing and subsequent shortage of spare engines worldwide. This has affected our operations due to grounding of aircraft and has impacted our ability to fully deploy capacity productively.”

To mitigate the problem, Elbers said that IndiGo is considering wet-leasing widebody aircraft and keeping older leased narrowbodies longer.

Other airlines reported to have been affected include India’s Go First and Airbus A220 operators Air Baltic and Air Tanzania. In December, the International Air Transport Association acknowledged the scale of the problem, warning that shortages of spare engines could weigh on industry profitability in 2023.

To ensure this does not happen, airlines need to prioritize spare-engine management and build their near-term fleet planning around it.

Related Content